The Real Reason to Hold On to Your Atlanta Rental (Even When Cash Flow Is Tight)

Key Points

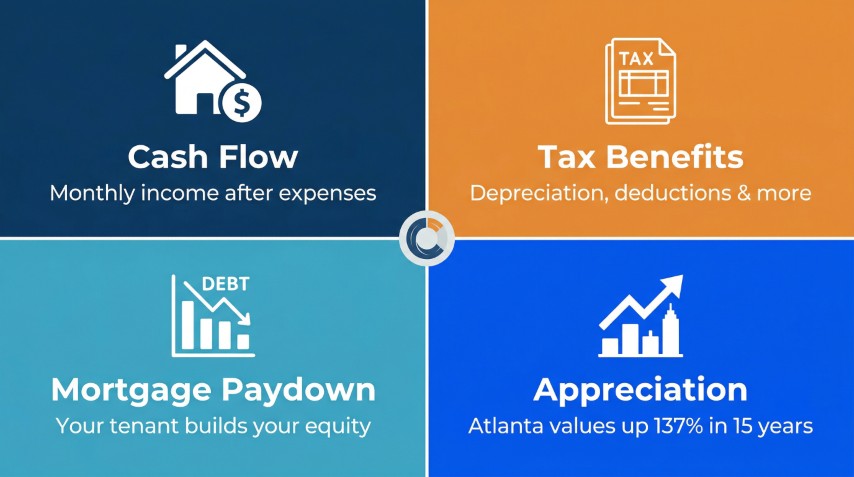

- Cash flow is only one of four ways rental property builds wealth.

- Atlanta homes appreciated 137.4% over the 15 years from 2010 to 2024, per FHFA data — an average of roughly 5.9% per year.

- Your tenant pays down your mortgage every month, whether you notice it or not.

- IRS depreciation creates a real tax deduction even when a property turns a profit.

- A $380K Atlanta rental with $100/month cash flow still generates $28,000–$39,000 in estimated total annual return.

Is $100 a Month Really Worth Keeping a Rental Property?

Yes, and the real return is much larger than what hits your bank account. Most landlords measure success by cash flow alone, which is understandable: it is the only return you can see in real time. But it accounts for a small fraction of what a rental property actually earns you.

Consider a $380K Atlanta home with tight cash flow of $100/month. That is $1,200 a year in visible income. Discouraging, right? Look at the same property through all four return pillars, and the picture changes completely.

Mortgage paydown adds roughly $3,500 per year in equity by year 5, paid entirely by the tenant. Atlanta appreciation has averaged close to 6% per year over the past 15 years, which adds $20,000–$30,000 per year on a $380K home. IRS depreciation saves $3,000–$4,000 per year in taxes. Combined, that property is generating $28,000–$39,000 in total estimated annual return on a $76,000 down payment. Cash flow was the smallest piece.

How Much Has Atlanta Real Estate Actually Appreciated?

According to the Federal Housing Finance Agency (FHFA), Atlanta-area home values increased 137.4% over the 15 years from Q1 2010 to Q4 2024. That works out to roughly 5.9% per year, compounded — and it includes the post-2022 cooldown when appreciation essentially flatlined. The 15-year window smooths out the COVID spike that distorts shorter-term figures.

To put that in concrete terms: the Atlanta median home price was roughly $159,000 in 2010. That same home is worth approximately $380,000 today — a $221,000 gain without lifting a finger. It required staying in the market.

Landlords who held through the 2006 downturn felt real pain in 2010, but those who did not sell recovered fully by 2015 and were up significantly by 2024, plus all the principal their tenants paid down in the meantime. The owner who sold in 2010 locked in a loss. The owner who held turned that same difficult period into one of the best wealth-building decades on record. Atlanta's long-term appreciation trend has rewarded patience consistently, even through market corrections.

What Is Mortgage Paydown and Why Does It Matter?

Mortgage paydown is the principal reduction on your loan that happens every month when your tenant pays rent. It builds equity silently. It never shows up as income, but it is real net worth.

On a $304,000 loan (20% down on a $380K home) at 6% over 30 years, the monthly payment is $1,823. The table below shows how equity accumulates over time:

| Year | Total Principal Paid |

|---|---|

| Year 1 | $3,733 |

| Year 5 | $21,115 |

| Year 10 | $49,595 |

| Year 15 | $88,012 |

None of this came out of your pocket. Your tenant covered every dollar. By year 10, you have $49,595 in additional equity you would not have if the property sat vacant or if you had sold. This return compounds alongside appreciation, not separately from it. That expense in year 2 that cost a few thousand and hurt at the time looks like a pretty good deal at year 5.

Can Rental Property Really Save Me That Much on Taxes?

Yes. The IRS allows you to depreciate a residential rental property over 27.5 years. On a $380,000 property with approximately $304,000 in depreciable value (land is excluded), that is roughly an $11,000 paper deduction every single year.

You did not spend that $11,000. No repair happened, no bill was paid. But it offsets your rental income on your tax return, which means you likely owe less even in profitable years. At a 28% marginal tax rate, that deduction saves roughly $3,100 per year. At 32%, it saves around $3,500. Some landlords in higher brackets save $4,000 or more annually.

Depreciation is the tax benefit most landlords underestimate, and it is one of the primary reasons real estate continues to attract serious investors even when cash flow is tight. Talk to your CPA about how depreciation applies to your specific situation.

What Does the Total Return Actually Look Like?

Here is what a realistic Atlanta rental scenario looks like when you account for all four return pillars, not just cash flow:

| Return Pillar | Annual Estimate |

|---|---|

| Cash flow ($100/month) | $1,200 |

| Mortgage paydown (Year 5 avg) | ~$3,500 |

| Atlanta appreciation (15yr avg ~5.9%/yr) | $20,000–$30,000 |

| Depreciation tax savings | $3,000–$4,000 |

| Total annual return (estimated) | $28,000–$39,000 |

That is a 37%–51% estimated annual return on a $76,000 down payment. From a property most landlords would describe as "barely breaking even."

Understanding what rental expenses actually look like is important context here. We covered the 30–40% expense ratio in detail in our post on what it really costs to rent out your home in Atlanta. Those costs are real. But they are also already baked into the cash flow number above, which means the other three pillars are pure upside on top of them.

When Does It Actually Make Sense to Sell?

Selling makes sense when you need the money soon, when the property has structural issues that make long-term holding uneconomical, or when a 1031 exchange into a better asset serves your goals. It does not make sense as a reaction to a few months of tight or negative cash flow.

Landlords who sell during hard patches consistently give up the largest gains. The data from Atlanta's 2006–2015 cycle is clear: the owners who held through the worst period came out significantly ahead. The ones who sold in 2010 absorbed losses they could never recover.

If expenses are higher than expected, the better question is usually whether the property is managed and priced correctly, not whether to exit the market entirely. If you know your property has significant deferred maintenance, structural problems, or systems issues that may surface sooner than later, selling may be the right move.

Frequently Asked Questions

Is rental property worth keeping if cash flow is low?

Yes, in most cases. Cash flow is one of four ways a rental property builds wealth — the others are mortgage paydown, appreciation, and depreciation tax savings. A $380K Atlanta rental with only $100/month in cash flow still generates an estimated $28,000–$39,000 in total annual return when all four pillars are counted.

How much have Atlanta home values appreciated over the last 15 years?

According to FHFA data, Atlanta-area home values increased 137.4% from Q1 2010 to Q4 2024 — roughly 5.9% per year, compounded. The Atlanta median was approximately $159,000 in 2010; that same home is worth around $380,000 today.

What is mortgage paydown and does it count as a return on rental property?

Yes. Mortgage paydown is the principal reduction that happens every month when your tenant pays rent. It builds equity you own outright. On a $304,000 loan at 6% over 30 years, your tenant pays down $49,595 of your principal by year 10 — none of which comes out of your pocket.

How does depreciation reduce taxes on a rental property?

The IRS allows residential rental properties to be depreciated over 27.5 years. On a $380,000 Atlanta home with roughly $304,000 in depreciable value, that creates an annual deduction of approximately $11,000 — saving $3,000–$4,000 per year in taxes at a 28–32% marginal rate, even in years the property turns a cash profit.

Fill out our Contact Form or call us at 678-389-3392. We will gladly help you understand what your home will rent for and give you the information you need to make an informed decision on whether or not renting makes sense for you.